Quickly Find Positive Cash Flow Properties Using Online Tools

With shares and managed funds still bouncing along the rocky road of volatility and uncertainty, many investors are looking to property investments now that the property market has begun to recover. This especially applies for people needing cash flows to support their retirement plans. Many people have been severely burnt by the declining value of their shares, lower dividends, losses to their superannuation nest-eggs, and failure of their self-funded retirement schemes.

For years many people have thought that investing in property would entail a weekly cost. This arise because many people in the past were focused on negative gearing and tax benefits, looking forward to capital gains to make a profit. But negative gearing means that you are making a loss, and getting tax benefits to cover that loss. Negatively-geared property investment relies heavily on capital gain - and you need large capital gains to cover for the losses over time. People often forget that you may have to pay capital gains tax on your investments. During times when inflation is high you will recover your losses, and get the tax benefits - but what happens if inflation remains low, as has been the case for the last 10 years or so?

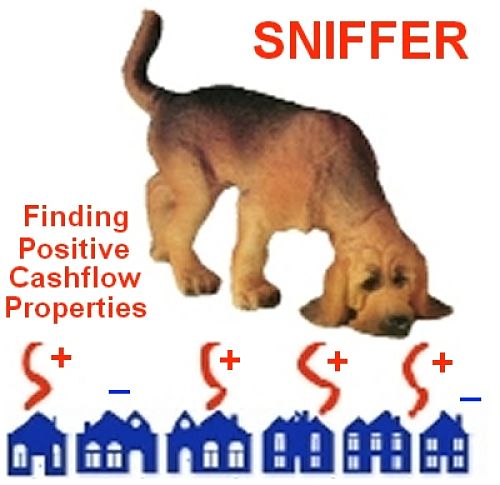

Using Sniffer the Online Positive Cash Flow Detector

The Positive Cash Flow Property Investment Strategy

The answer to a fundamental shift in strategy from Negative to Positive Cash Flow. Now you will be looking for properties that give you a cash return now, and not be reliant on future capital gains, but you can get these benefits as well. You will be looking for properties that put cash in your pocket, every week, from the day you buy it. This new concept will require a different strategy and considerable research before you invest.

There are several ways to generate positive cash flows from property investments.

- Positive Gearing - You will need to find property that has high rent returns in relation to the purchase price and will cover all the expenses on the property, including mortgage and maintenance costs and will leave you some cash to pocket . The net gain from the rent less the costs may then be seen as income and be taxed. Typically, these properties are flats and apartments in regional areas where building costs are low, there is a shortage of rentals properties and lots of people wanting to rent, perhaps because of some type of development.

- High Deposits - You may also generate a positive cash flow but investing a higher amount in the property as a cash deposit, thereby reducing your mortgage and borrowing costs.

- High Deductions - This can occur where a property has been recently renovated or may otherwise have a whole host of depreciable items. When you claim both high expenses as well as depreciation , to you tax breaks you will be looking for properties where these benefits outweigh the costs in terms of loan interest, rental costs, rates, body corporate fees, etc).

Positive cash flow totally changes your investment strategy. If say the weekly costs for a property are $50 a week (after tax), then what limits the number of properties you can buy is your disposable income. But, if a property gives you a cash return of $50 a week, then what limits how many properties you can buy is your existing equity, or cash available, and your ability to borrow money. Also cash in your pocket means you can pay off your debt more quickly and borrow more money as the cash can cover extra loans. You will soon be in the position to buy more property. In contrast cash out of your pocket will greatly slow down your debt repayment.

How can you Find these Positive Property Cash Cows?

Finding positive cash flow properties that you can invest in is not easy,especially when you start, because you will have to totally change where to look for and what to look for. Some of key point about looking for these properties are:

- New or near-new property of any type to benefit from depreciation benefits.

- Properties in regional areas where capital growth has been suppressed, but where the rental markets are booming because of regional developments.

- Blocks of flats and apartments are likely to have lower net costs for each unit compared with the rent returns.

- Apartments and town house which you can buy off the plan at greatly reduced cost.

- Houses and apartments in holiday areas where the vacation rents may be very high, provided this rental can be sustained.

- Look at debt funded Positive Cash-flow options - This requires careful decisions, but provided the cash flow is real and sustained this can be very rewarding especially if you have a lot of equity in other properties to support your borrowing.

- Check the rental and property values, especially in regional area. These statistics are available in many magazines. Also trawl the net looking for relatively high rents in relation to costs. But remember that the rents in regional areas may appear to be low, but what matters is the rent size in relation to the cost of the property.

- Look for ‘Unusual’ properties such as multi-occupancy offering, properties with 'granny-flats', single wall dwellings, etc.

- Look In Rural Towns where it may be still cheaper to rent than to buy, which means their cost will be depressed.

- Consider creating a Positive Cashflow Property. There are many ways you can take a negatively geared property and make it positive. For example you may renovate and increase the rent, or provide better facilities in return for increased rent. You could buy land and build an apartment complex or hotel. You could buy land, subdivide it, sell off some of it so that the net price you pay for the land you build your flats on is much lower.

What Software Systems and Online Tools are Available?

There are many and varied software options and online tools. Perhaps the simplest is often the best especially for an initial search.

Sniffer - An Online Tool for Finding Positive Cash Flow Properties

About Sniffer

For this online tool all you need to enter are:

- Number of Flats (1 = house)

- Purchase Price

- Total Loan Required

- Deposit paid

- Mortgage Required (Calculated)

- Interest Rate

- Loan Period (Years)

- Total Rent per week (Sum for all flats).

Built-in simple cost estimates are applied to stimulate the expected returns from renting the property - units, apartments, house or flats. These cost estimates are based average costs for a wide range of properties This includes management fees, rates, repairs and maintenance, grounds/mowing/gardens, insurance, land tax , loan costs, other costs - postage etc. The total net overall cost for the property is the sum of the costs less the total depreciation. These costs are displayed as 'Net Cost' on 'Sniffer'. The package does not consider tax benefits, capital gain, general loan costs, negative gearing and interest-only loans, etc., and many other issues. It is a very simple package but it has a lot of benefits for a quick check ('sniff') to look for properties that deserve more detailed scrutiny.

Sniffer calculates:

- Loan Repayments

- Rent (monthly)

- Net Costs (monthly) - The estimated total costs for the property.

- Rental Return (monthly) - The net monthly return is the monthly rent, plus depreciation allowance, less the total costs each month.

- Cash Flow each Month ( for 100% mortgage ) - The net cash flow estimate is the total return (rent+depreciation-costs) less the monthly mortgage repayment. In this case it is cash flow expected when you have borrowed money for the entire mortgage (for 100% of the price)

- Cash Flow each Month ( for 90% mortgage ) - This is the cash flow expected after paying loan costs for 90% of the original loan. This allows you to see the effect of paying off and extra10% of the loan, either at purchase or during the repayment period.

- Cash Flow each Month ( for 80% mortgage ) - This is the cash flow estimate after paying for 80% of the original loan.

- Cash Flow each Month ( with No mortgage ) - This is the cash flow expected if you had paid the full price for the property and there were no loan repayments.

- Yield (the rent related to price) - This yield is the gross rent income each year, expressed as a percentage of the original purchase price.

- Yield (the rent related to mortgage) - This yield is gross net rent income per year expressed as a percentage of the mortgage loan.

- Yield ( as cash flow - no mortgage related to price) - This yield is the net cash flow (with no mortgage repayments) per year, expressed as a net percentage of the purchase price.

Finally the package shows a set of scores for the range of mortgage levels and using a simple indicators - 'Red', 'Orange' and 'Green'. This provides an instant guide for the cash flow potential of the properties with 'Green' indicating the properties that have positive cash flow now and 'Orange', those that are close to being positive. 'Red' signifies properties not worth considering.

Conclusion: Using online tools such as 'Sniffer' can provide a great way to quickly find potential positive cash flow properties, that you can research further with better cost estimates. It gives you various options in terms of how much cash you need to put down as a deposit to get the positive cash flow returns that you need. Using these tools in combination with the strategy outlined above provides a unique path for financial independence. This is a good option to consider as an alternative to shares, managed funds or superannuation.